Mega‑funds operate under brutal math.

A $8B fund needs roughly $24B in returns to hit a 3x. With typical ownership ranges between 10 and 20% , it means that the portfolio must generate between $120B and $240B in exit value.

It’s easy to see how it requires massive hits (Figma, Wiz, EA, CyberArk etc) to achieve these numbers. Everything else is noise.

Because the entire fund depends on a few companies, anything that delays or damages those exits hits the fund’s IRR hard.

Why Security Matters: The IRR Sensitivity

IRR is annualized return rate of an investment, taking into account the timing of cash flows.

It tells you what percentage return is effectively earned per year, after considering when money went in and when money came out.

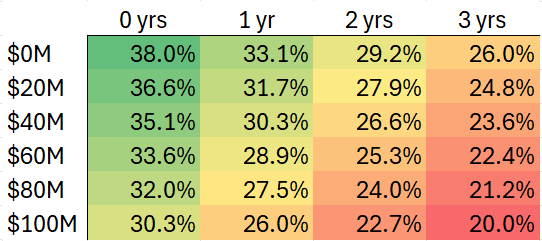

IRR is hypersensitive to time. A simple example:

- Invest $50M

- Exit $500M in Year 7 → ~38% IRR

Now introduce security friction:

- 1‑year delay (same valuation): Exit in Year 8 → 33% IRR A 5‑point drop just from time.

- 2‑year delay: Exit in Year 9 → 29% IRR -> a 24% reduction in performance.

- $20M breach cost (no delay): Exit $480M in Year 7 → 36.6% IRR Costs hurt, but not like delays.

- Delay + cost (the realistic case): Exit $480M in Year 8 → 31% IRR

Combine the two and a recipe for disaster is served. This is why late‑stage investors treat security as an exit‑risk variable, not a technical detail.

How Mega‑Funds Price Security Risk

Mega‑funds rarely say “your security posture is weak,” but they absolutely price it in. It shows up in four places:

1) Valuation Haircuts

Security gaps quietly reduce valuation. For example:

- 5–15% for missing compliance

- 15–30% for known gaps

- 30–50% if there’s been a breach

They don’t argue about it; they just lower the number.

2) Ownership Demands

If they think exit timing is risky, they compensate by taking more of the company. More ownership = IRR buffer.

3) Governance Requirements

Usually seen when security looks shaky:

- “Hire a CISO within 3 months”

- “SOC 2 Type II required before next raise”

- “Quarterly security reporting to the board”

- “Mandatory third‑party audit”

These are not suggestions. They’re conditions. “Performative security” is the enemy here, where showing action is perceived as more relevant than the outcomes of the action itself.

4) Deal Structure

If risk is high enough:

- tranched investments

- enhanced liquidation prefs

- redemption rights

- discounted warrants

Security is one of the few issues that can push a clean deal into structured territory.

Why This Matters at the Fund Level

A mega‑fund might have 40–60 portfolio companies, but only 3–5 matter, and 1–2 carry the entire fund.

If one of those winners hits a security‑driven delay:

- the exit slips 12–24 months

- valuation gets cut

- burn increases

- a down‑round dilutes ownership

- IPO readiness gets pushed out

A single delayed exit can drag a fund from 15% IRR → 10%, which is the difference between “top‑quartile” and “don’t raise another fund.”

This is why mega‑funds are (or should be) ruthless about security posture.

How Founders Can De‑Risk Security Before Fundraising

Here’s the practical playbook founders use to avoid valuation haircuts and governance penalties:

1) Get the basics done early. For example:

- Security (and Privacy when relevant) by Design

- Governance frameworks in place.

- Clean cloud architecture (CSPM tools help)

- Clear access control model

- MFA everywhere

- Pen test from a reputable firm

- Documented incident response plan

- Centralized logging + monitoring

This signals maturity without slowing you down.

2) Show a real security owner

It doesn’t have to be a full‑time CISO at Series A/B; a credible security lead / vCISO / fractional CISO is enough to calm investors. However s/he must bear sufficient authority (and budget) to carry on the things in #1.

3) Demonstrate enterprise readiness

If you want enterprise revenue, you need:

- SOC 2 Type II / ISO 27001 / whatever required by the regulatory space you happen to hit.

- Vendor security questionnaire responses (as a minimum), plus more tailored (and stringent) approaches for your critical supply chain.

- Data governance basics

Enterprise customers are the fastest way to $100M ARR — and the fastest way to blow up a deal if your security is weak.

4) Avoid “security debt cliffs”

The worst scenario is when a company tries to fix 5 years of security debt in the 6 months before a Series C or IPO. Investors can smell this panic.

5) Pre‑empt diligence

Before fundraising, prepare:

- a clean security posture summary

- compliance roadmap

- architecture diagrams

- pen test results

- list of remediated issues

This flips the script: instead of investors discovering problems, you show them you’re already on top of it.

The Bottom Line

Security isn’t about perfection — it’s about predictability.

Mega‑funds need confidence that you:

- won’t blow up an exit

- won’t delay an IPO

- won’t lose enterprise customers

- won’t force them into structured deals

- won’t tank their IRR

A founder who can show a credible, proactive security posture gets:

- better valuation

- cleaner terms

- faster closes

- stronger follow‑on support

And most importantly: they avoid becoming the company that drags down a $8B fund because of a preventable security delay.